How are we doing?

The UK Water Industry Research Limited, UKWIR, developed a standardised workbook & associated methodology for estimating Operational greenhouse gas, GHG, emissions, called the Carbon Accounting Workbook, CAW, to bring consistency and accuracy to the reporting process across the water industry.

The workbook has been in place for over ten years and is annually reviewed to incorporate the latest best practice and science regarding estimation & reporting of greenhouse gas emissions and is updated accordingly.

Separately from the CAW, Welsh Water have undertaken their own estimates & studies on the emissions associated with the purchase of Capital Goods & Services (embedded carbon) and the carbon emissions that are currently sequestered from company owned land holdings.

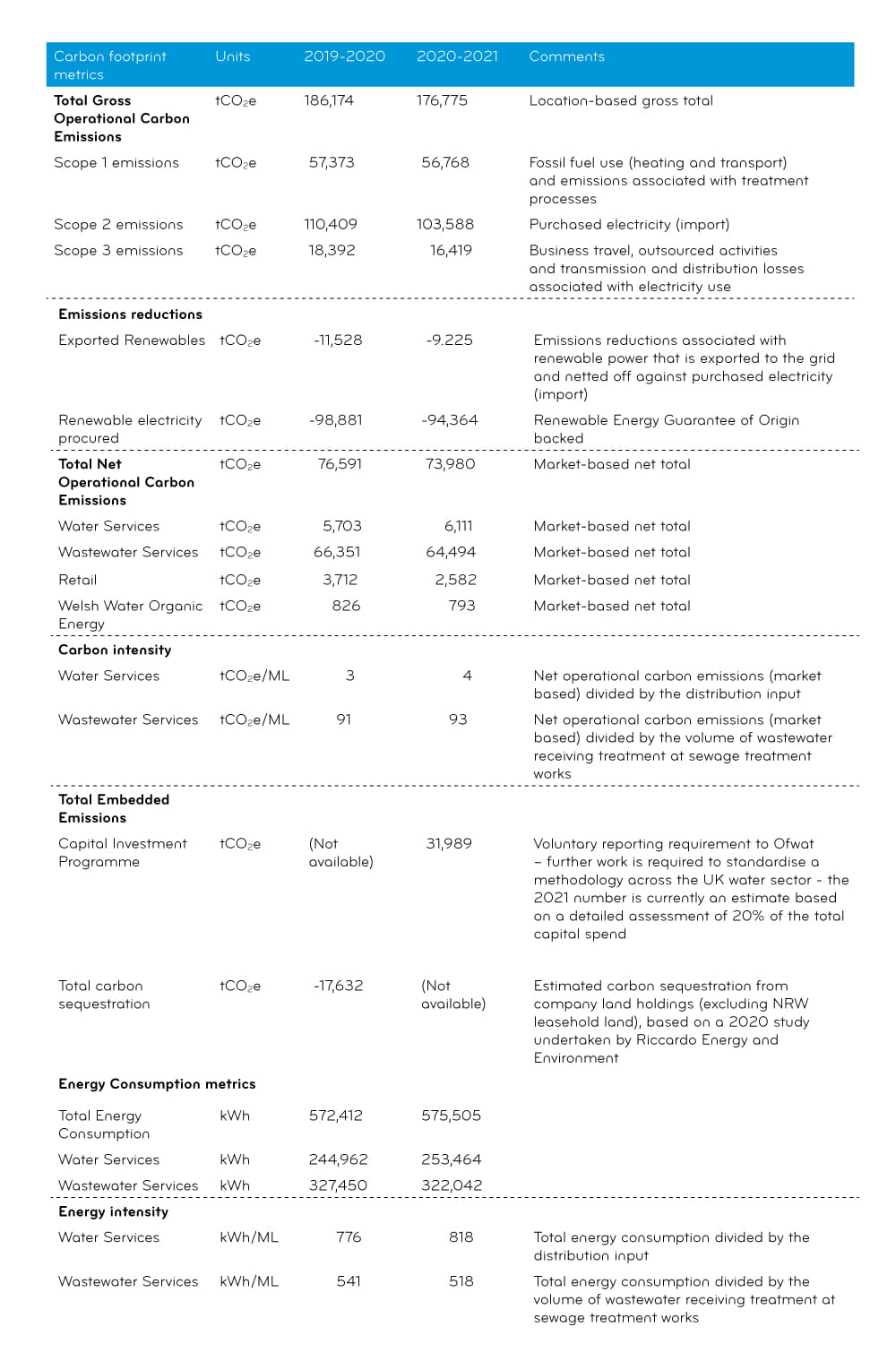

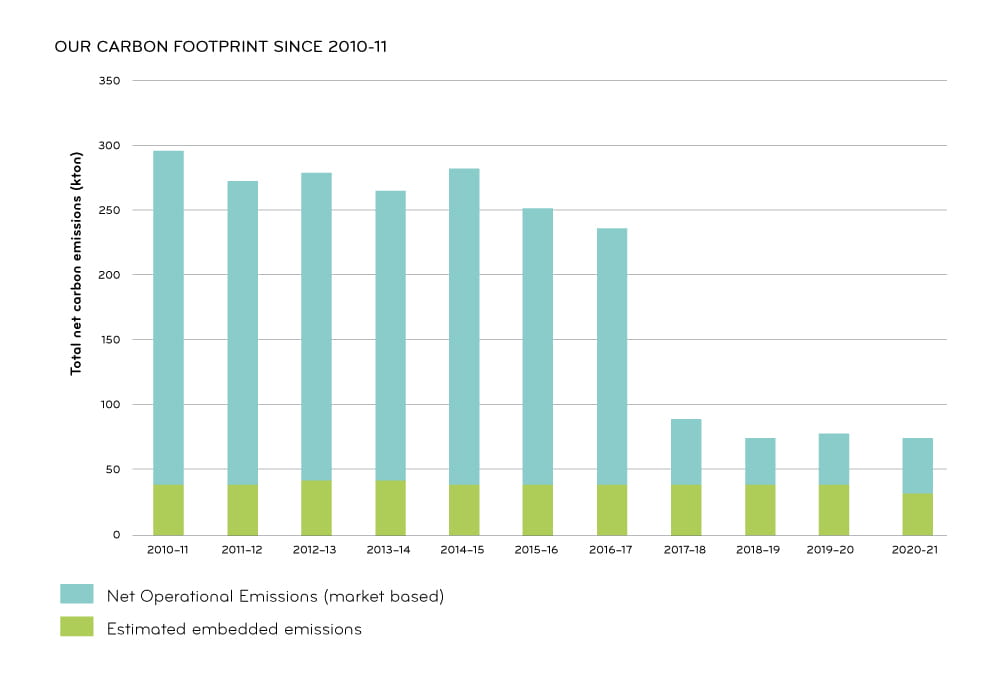

The Table and graph below shows the 2020-2021 emissions numbers that have been reported in our annual report and to Ofwat (the industry economic regulator):

| Definition: | Welsh Water main emission sources | ||

|---|---|---|---|

| Scope 1 | Direct Emissions | Scope 1 emissions are direct greenhouse (GHG) emissions that occur from sources that are controlled or owned by an organization (e.g., emissions associated with fuel combustion in boilers, furnaces, vehicles) |

|

| Scope 2 | Indirect Emissions | Scope 2 emissions are indirect GHG emissions associated with the purchase of electricity, steam, heat, or cooling. |

|

| Scope 3 | Indirect Emissions | Scope 3 emissions are all indirect emissions (not included in scope 2) that occur in the value chain of the reporting company, including both upstream and downstream emissions. |

|

Operational emissions represent the carbon emissions association with all their day-to-day activities that Welsh Water undertake on a daily basis to serve its customers. These emissions numbers exclude the embedded carbon, i.e. upstream emissions associated with the purchase of (capital) goods.

Location based accounting method represent the carbon footprint taken at the average emissions intensity of grids on which energy consumption occurs (using mostly grid-average emission factor data). A market-based method reflects emissions from electricity & natural gas that companies have purposefully chosen. As such the market-based method reflects the emissions from the electricity & bio-methane that a company is purchasing (backed by Guarantee of Origin’s), which may be different from the electricity that is generated locally. It’s good practice to report both Location-based and market-based numbers.

Gross emissions are your total GHG emissions (location-based or market-based) before accounting for any emission reductions that are associated with the export of electricity or bio-methane to the grid, whereas Net emissions include the reductions associated with these exports.

Carbon sequestration is a natural or human (artificial) process of capturing and storing atmospheric carbon dioxide. It is one method of reducing the amount of carbon dioxide in the atmosphere with the goal of reducing global climate change and requires the long-term storage of carbon in plants, soils, geologic formations, and the ocean.